The Numbers That Nobody Wants to Discuss

Open a browser in Lagos, Nairobi, or Johannesburg during Premier League weekend, and the digital landscape tells a story nobody in the development community wants to tell: sports betting platforms are moving more money than most African banks. Betway, Hollywoodbets, and a dozen regional competitors command more daily traffic than LinkedIn, than professional job sites, than e-commerce platforms. They are not peripheral to the African internet economy. They are central to it.

The data is staggering. In South Africa alone, sports betting operators collectively handle over R20 billion (approximately $1.1 billion USD) annually. Nigeria’s betting market is estimated at over $2 billion. Kenya, Uganda, Tanzania—the pattern is consistent across the continent. These are not side bets. These are primary destinations for discretionary spending.

And the customers are disproportionately young, male, and unemployed or underemployed.

Need a Freelancer for This?

Hire verified talent on Fiverr — starting from $5. No contracts, no hassle.

Browse Fiverr Freelancers →The conventional narrative frames this as a social problem: “Gambling addiction in Africa is out of control.” “Youth are wasting their money on bets.” “We need tighter regulation.” All true. But this framing misses the deeper economic issue, which is less a problem of morality than of capital allocation.

The real question is not whether African youth are gambling too much. It is why capital that could be pooled into productive investment is instead flowing through betting platforms and disappearing into the operating margins of foreign-owned corporations.

How Betting Platforms Captured Sports Betting Africa vs Investing Income

To understand this, you have to understand what happened after 2010 in African telecommunications.

When mobile money—M-Pesa, MTN MoMo, Airtel Money—made instant payments frictionless, it opened a new frontier for financial services. Young people who had never had a bank account suddenly had a way to send money instantly, in any amount, at any time. The assumption among development economists was that this would drive entrepreneurship, savings, and investment.

What actually happened was that betting platforms, already massive in developed markets, recognized an opportunity.

A young person in Kampala could now place a bet on an English Premier League match in 30 seconds. No paperwork. No questions. No minimum balance. The payouts—when you win—are instant and frictionless. The marketing is culturally targeted: football is the lingua franca of African youth. Sports betting platforms don’t sell gambling. They sell the fantasy of winning, told through the language of the sport that matters most.

The product design is ruthless. Platforms offer “multi-bets”—parlays that let you combine 5, 10, sometimes 20 individual bets into a single ticket. The odds multiply. A $1 bet can theoretically pay out $10,000. The probability of winning is microscopic. But the psychological appeal is overwhelming: a small bet, an enormous potential return, and the illusion of control through “strategic” bet selection.

The platforms know the math. They are built to extract wealth, not to distribute it.

Yet young Africans engage with these platforms with a seriousness they rarely apply to other financial products. They study form. They follow odds movement. They have WhatsApp groups where they share “tips” and “sure bets.” The time and attention invested rivals that of any financial analyst.

The difference is that bookmakers have a mathematical edge. Over time, everyone loses.

The Math of Expected Value

Let me be precise about what “losing” means.

Betting platforms operate on negative expected value for the player. If you place a $10 bet at 2-1 odds, you’re risking $10 to win $20. The platform calculates the probability you assign to that outcome. If the true probability of winning is 40%, then your expected value is:

- Expected Value = (Probability of Win × $20) + (Probability of Loss × -$10)

- Expected Value = (0.40 × $20) + (0.60 × -$10)

- Expected Value = $8 – $6

- Expected Value = $2

So on average, per $10 bet, you make $2. Over 1,000 bets, you’d expect to win $2,000.

But the platform doesn’t price bets at true probability. It prices them at true probability minus the house edge. The house edge on most bets is 5-10%. So the actual expected value for the player is negative.

Expected Value (with 7% house edge) = -$0.70 per $10 bet

Over 1,000 bets, you expect to lose $700.

Now extrapolate. A young person in Nigeria placing 20 bets per week for a year is placing 1,040 bets. At an average stake of $2-5, that’s between $2,080 and $5,200 per year. With a 7% house edge, the expected loss is between $146 and $364 per year.

For someone earning $200-400 per month (the reality for many African youth), this is not a “loss.” It is a tax on hope.

What That Money Could Actually Do: The Capital Pooling Alternative

Now consider an alternative scenario.

Imagine if those same young people pooled that capital into a rotating savings and loan association—what Africans call a merry-go-round, susu, or accumulating savings and credit association (ASCA). This is an ancient and proven financial instrument.

Here’s how it works:

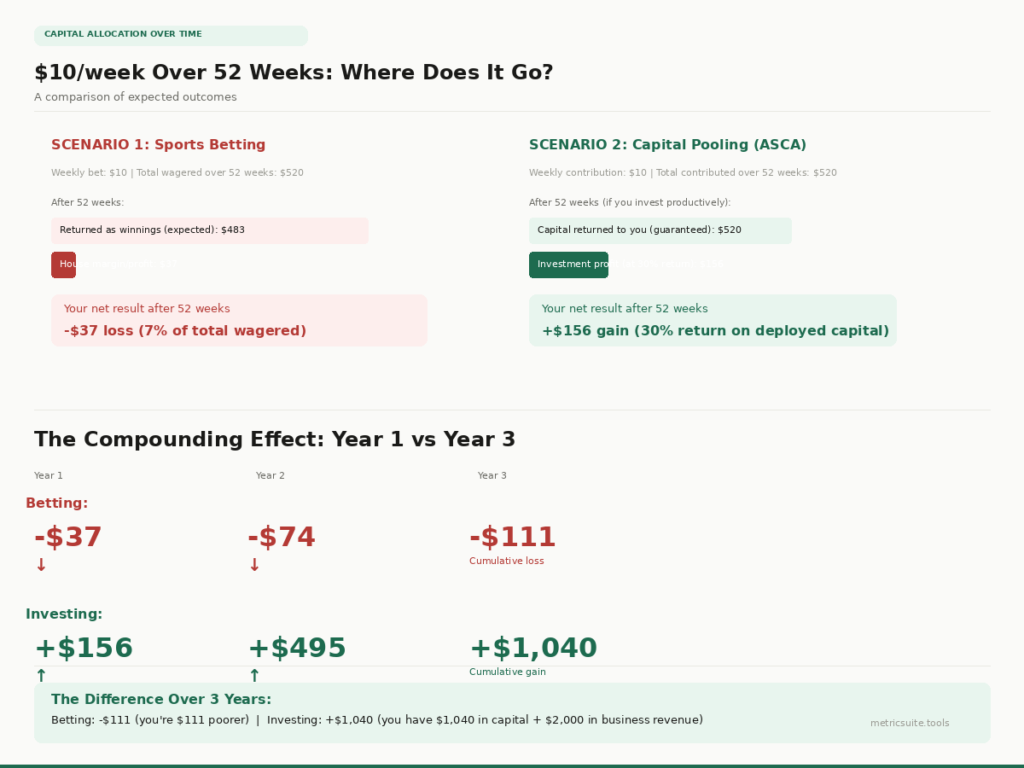

Twenty young traders agree to contribute $10 each per week. That’s $200 in capital per week. Every week, one member receives the full $200. After 20 weeks, every member has received $200, and the cycle completes.

But now imagine they add a condition: you can only receive your $200 if you have a documented business plan and at least 3 months of business financials showing profitability.

The same young person who was betting $10 per week is now part of a group that controls $200 in loanable capital. After the first cycle, they have access to a $200 working capital loan at 0% interest. They use it to import goods for resale. Over 3 months, they generate $300 in profit (a healthy 50% return on capital). They pay back the $200, keep the $100 profit, and contribute to a second cycle.

After 12 months, they have accumulated $400 in capital and are part of a network that controls $4,000 in circulating credit. They have not become wealthy. But they have become economically active.

Compare this to the betting scenario: after 12 months, they have lost $700-1,000 and are no better off than they started.

The difference is not luck. It is the difference between negative expected value and positive expected value. Between extractive financial products and productive ones.

The Business Model Behind the Betting Platform

Let’s talk about who wins.

Betway, Hollywoodbets, and other major platforms are not African companies. They are UK and European-listed businesses with operational bases in Africa. The profits generated in Nigeria, Kenya, South Africa, and Uganda flow out of the continent to shareholder dividends and corporate headquarters in London and Malta.

This is not incidental. This is structural.

In 2021, a UK government report estimated that the global sports betting market was handling £370 billion in wagers annually, with an estimated £15 billion in operator profit margins. The industry’s business model is simple: take bets, pay out less in winnings than you collect in stakes, and keep the difference as margin.

For the operating platform, there is no risk. The platform makes money regardless of match outcomes because it matches bets: for every bettor backing Liverpool, there is another backing Manchester United. The platform’s only risk is if a particular outcome is so heavily bet-on that payouts exceed stakes.

This is called an “imbalanced book.” But betting platforms have solved this through sophisticated algorithmic pricing. Odds shift in real-time to incentivize action on the underbet side. The platform’s margins stay locked in.

From an African perspective, this is a wealth extraction mechanism. Capital flows in. Only a fraction flows back as winnings. The rest becomes profit that leaves the continent.

Why Youth Choose the Bet Over the Business

This analysis assumes rational economic actors making calculated decisions. In reality, the choice of betting over investing is not rational. It is psychological.

First, betting offers immediate feedback and instant gratification. You place a bet on Sunday. By Monday evening, you know if you won or lost. A business investment takes months or years to show returns. The psychology of immediate feedback is powerful.

Second, betting requires no skills or knowledge to enter. Placing a bet takes 30 seconds. Starting a business requires planning, capital, suppliers, customers, accounting. The barrier to entry is vastly higher.

Third, betting platforms invest billions in marketing, and this marketing is specifically designed for African youth. Betway sponsors African football clubs. Hollywoodbets runs ads during Champions League broadcasts. The message is constant: “Your luck can change in 90 minutes.”

Fourth, and most importantly, unemployment and underemployment make betting feel like a rational response to an irrational economy. If you are a college-educated 23-year-old with no job prospects, the expected value of your education is negative. Under those conditions, betting on a 100-1 parlay is not irrational. It is a rational response to a system that has already written you off.

This is the critical insight that changes the entire analysis: betting is not the cause of African youth unemployment. It is a symptom.

Betting platforms are not creating the desperation. They are exploiting it.

What MetricSuite Represents in This Context

The tools on MetricSuite.tools—the Wholesale vs Retail Pricing Optimizer, the Crop Profit Calculator, the Social Commerce Profit Tracker—exist precisely because the alternative to betting is not just “don’t bet.” The alternative is accessible business tooling.

An unemployed trader in Lagos cannot start a business without understanding her landed costs. A diaspora farmer cannot commit capital to crops without calculating ROI. A WhatsApp seller cannot scale without tracking profit per unit. These are not luxuries. They are the infrastructure of productive entrepreneurship.

Betting platforms have mobile apps. They have zero friction. They have billions in marketing spend.

Productive investment infrastructure in Africa is fragmented, expensive, and often inaccessible to the young and underemployed.

This is a systemic problem, not an individual one. The solution is not to shame young Africans for betting. It is to build better alternatives.

The Policy Question Nobody Wants to Ask

Most African governments, when confronted with the betting boom, pursue regulation: licensing requirements, tax increases, responsible gambling warnings. These are necessary. But they miss the point.

Institutions like the African Development Bank have spent decades funding SME financing and youth entrepreneurship programs across the continent — the real infrastructure question is whether that capital reaches the same young person currently being marketed to by betting platforms.

Regulation of betting platforms will not redirect capital toward productive investment. It will only reduce the platforms’ profitability and competitiveness. The capital will not automatically flow toward capital pooling or business investment. It will simply stop flowing.

The real intervention would be to make productive investment as frictionless as betting:

- Regulated capital pooling platforms — Digital ASCA networks where young people can pool capital with algorithmic matching of savings groups. Governments could provide tax incentives for participation.

- Business microcredit at betting platform speeds — Instant micro-loans (under $500) for documented business ideas, approved in minutes instead of weeks.

- Financial literacy integrated into platforms — Betting platforms show odds. Why don’t they also show expected value? Why don’t they show, in real-time, how much money the player has lost?

- Productive asset betting — This is speculative, but: what if you could place bets on African agricultural commodities futures? Bet that maize prices will rise, that palm oil will fall? This would at least connect speculation to productive markets rather than sports outcomes.

None of these require banning betting. They require building something better.

The Uncomfortable Truth

The reason sports betting platforms are winning is not because they are evil (though their business model extracts wealth). It is because they understood something development economists missed: young Africans want agency. They want to control their economic destiny. They want to feel like they matter.

Betting platforms offer that feeling. It is a false feeling. But it is a feeling nonetheless.

The alternative is to build real systems where young Africans can actually control their destiny: business tools that work for them. Capital pooling networks that give them access to credit. Investment infrastructure that is as mobile, as frictionless, and as culturally integrated as the betting platforms they now use.

Until that infrastructure exists, the capital will continue to flow toward odds and away from opportunity.

FREQUENTLY ASKED QUESTIONS

Q: Aren’t you just saying betting is bad and business is good? Isn’t that simplistic?

A: Yes and no. I’m not arguing that betting is morally bad. I’m arguing that from a pure expected-value perspective, betting has a negative expected value for the player and a positive expected value for the platform operator. Business investment has a positive expected value for the entrepreneur and creates economic activity. The comparison is about capital allocation, not morality. That said, the psychological appeal of betting—immediate feedback, low barrier to entry, fantasy of transformation—is real. The solution is to build business tools with those same characteristics, not to judge people for preferring them.

Q: Isn’t rotating savings and loan associations (ASCAs/merry-go-rounds) just betting with a different name?

A: No. In an ASCA, all the capital contributed by members is returned to members. The payout is guaranteed. There is no house edge. There is no wealth extraction. The expected value is zero for the group and positive for the most entrepreneurial members who can deploy the capital productively. In contrast, betting has a negative expected value for players. This is not a philosophical distinction. It’s a mathematical one.

Q: If betting is so profitable for the operators, why don’t African entrepreneurs build competing platforms?

A: Some try. But there are significant barriers: licensing requirements (which vary by country), regulatory complexity, and the fact that the existing platforms (Betway, Hollywoodbets, etc.) have massive first-mover advantages. An African entrepreneur could build a betting platform, but they’d be competing in a global market with established players. What they could do is build capital pooling platforms, investment apps, or business tools—areas where there is less competition and less regulatory friction. MetricSuite.tools is an example of this: tools for entrepreneurs, not for extraction.

Q: Aren’t you ignoring the fact that some people actually win at betting?

A: Yes, some people do. But they are the exception, not the rule. For every bettor who wins significantly, thousands lose. The mathematics of a negative expected value means that even if you are skilled, you must be skillful enough to overcome the house edge. For sports betting, this is extremely difficult. There are professional bettors, but they are rare and typically deal in large volumes and are arbitraging inefficiencies in pricing, not predicting outcomes. For the average young person in Africa, the probability of being a successful bettor is negligible. The documented expectation is a loss.

Q: What is your actual policy recommendation?

A: Three things: (1) Transparency: betting platforms should show expected value to customers in real-time, the same way they show odds. (2) Alternative infrastructure: governments and impact investors should fund digital capital pooling platforms and micro-lending systems that operate at betting platform speed. (3) Financial literacy: teaching expected value, compound interest, and capital allocation should be standard in African schools. You cannot solve a financial behavior problem without addressing financial literacy.

Q: How does this connect to the Wholesale vs Retail Pricing Optimizer tool you mentioned?

A: The tool is an example of what betting platforms are not. It doesn’t extract wealth. It helps traders make better decisions and keep more profit. It requires engagement (you input data), it has an educational component (you see cost breakdowns), and it has a positive expected value for the user. This is the model we should scale: tools that align user incentives with productive economic activity.