The Rise of African Entrepreneurship and the Enormous Inter-Africa Trade Opportunities You Cannot Afford to Ignore

There is a revolution taking place across the African continent, and it is not being televised. It is not being led by governments, multinational corporations, or foreign aid agencies. It is being led by entrepreneurs, millions of them, operating from Lagos market stalls, Nairobi co-working spaces, Cairo apartment kitchens, Accra WhatsApp groups, and Johannesburg garage workshops. And for the first time in modern history, these entrepreneurs are beginning to trade with each other across borders at a scale the continent has never seen.

This is not speculation. This is the single most significant economic shift on the African continent in the post-independence era.

The numbers tell a story the world is ignoring

Intra-African trade has historically been shamefully low. For decades, African nations traded more with Europe, China, and the United States than with their own neighbours. In 2019, intra-African exports accounted for roughly 17 percent of the continent’s total exports, compared to 68 percent for Europe and 59 percent for Asia. Africa was, in economic terms, a collection of outward-facing economies designed during the colonial period to extract raw materials and ship them north.

Need a Freelancer for This?

Hire verified talent on Fiverr — starting from $5. No contracts, no hassle.

Browse Fiverr Freelancers →That architecture is finally cracking.

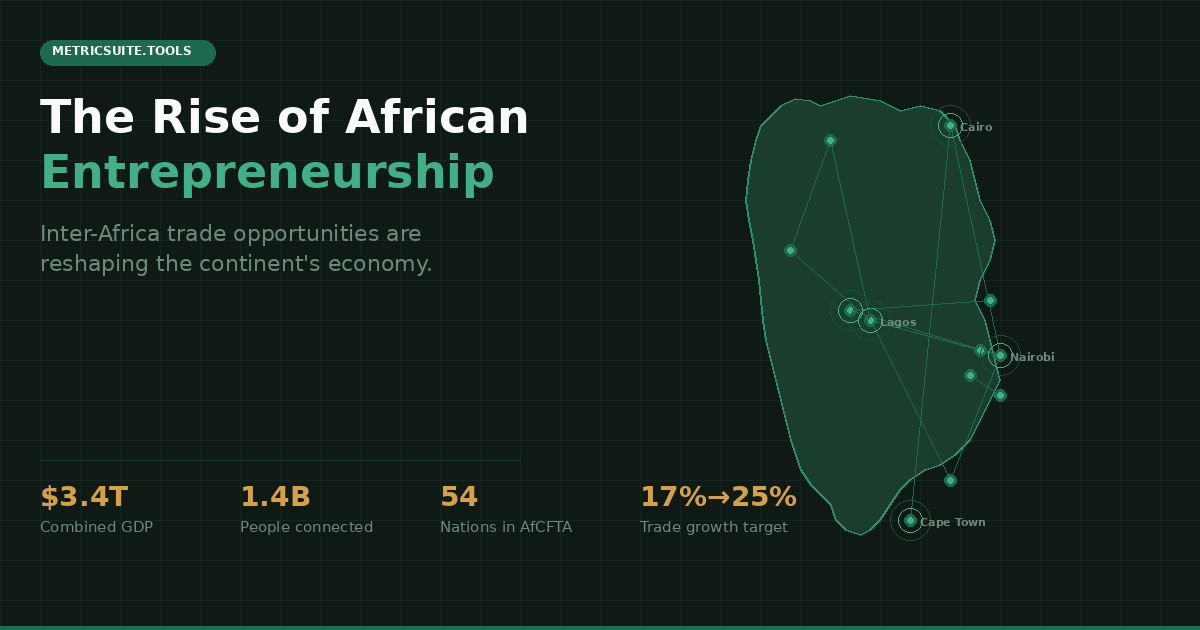

The African Continental Free Trade Area, known as the AfCFTA, entered its operational phase in 2021 and now connects 54 countries and 1.4 billion people into what is, by number of participating nations, the largest free trade area in the world. The United Nations Economic Commission for Africa estimates that the AfCFTA has the potential to increase intra-African trade by between 15 and 25 percent by 2040, representing tens of billions of dollars in new commerce. The African Development Bank projects that the agreement could lift 30 million people out of extreme poverty.

But here is what the institutional reports consistently miss: the AfCFTA is not just a policy framework. It is an entrepreneurial opportunity of historic proportions, and the entrepreneurs who understand this first will be the ones who build the next generation of African businesses.

The entrepreneur is the engine, not the government

Pan-Africanist thinkers from Kwame Nkrumah to Cheikh Anta Diop to Thomas Sankara understood that political independence without economic sovereignty is an illusion. What they perhaps could not have foreseen is that the vehicle for this economic sovereignty would not be the state-run enterprise or the five-year development plan, but the informal trader with a smartphone, a WhatsApp Business account, and the determination to sell across borders.

Consider the reality on the ground today. A woman in Kigali manufactures handmade leather bags. She sells them locally, but she knows there is demand in Abidjan, Nairobi, and Johannesburg. Before the AfCFTA, she would face different tariff regimes in each country, with rates sometimes exceeding 20 percent. Today, under the agreement’s preferential tariff schedules, many of those rates are being reduced or eliminated entirely. The question she faces is no longer whether cross-border trade is viable, but whether she can calculate the actual cost of doing it.

This is where the practical meets the political. It is not enough to celebrate the AfCFTA as a Pan-African achievement, which it is. The entrepreneur needs to know: what is the preferential tariff rate for leather goods from Rwanda to Côte d’Ivoire? What are the rules of origin? What documentation is required? These are answerable questions, and tools like the AfCFTA Tariff Lookup Tool exist precisely to make this information accessible to the small business owner, not just the corporate trade compliance department.

The mobile money revolution changed the game

You cannot understand the rise of African entrepreneurship without understanding mobile money. When M-Pesa launched in Kenya in 2007, it did something that decades of banking sector reform had failed to do: it gave ordinary people a way to send and receive money instantly, without a bank account, without paperwork, without permission from anyone.

Today, Sub-Saharan Africa accounts for nearly 70 percent of the world’s billion-dollar mobile money transaction volume. M-Pesa, MTN MoMo, Airtel Money, Orange Money, Wave; these platforms are the financial infrastructure of African entrepreneurship. They are how the Lagos fashion designer receives payment from a customer in Port Harcourt. They are how the Kampala coffee exporter gets paid by a buyer in Dar es Salaam. They are how the Cairo freelancer receives earnings from a client in Casablanca.

But here is the problem that nobody in Silicon Valley is solving: the fee structures across these platforms are opaque, inconsistent, and vary dramatically by corridor. Sending money from Kenya to Uganda on M-Pesa costs a different percentage than sending it on Airtel Money. Withdrawing to a bank account costs differently than withdrawing to cash. For an entrepreneur making dozens of transactions a week, these fees compound into a significant erosion of margin, and most people have no easy way to compare them before choosing a provider.

This is exactly the kind of gap that the Mobile Money Fees Comparison tool was built to address. Not as a theoretical exercise, but as a practical calculator that lets a business owner input a transaction amount, select a corridor, and see the actual fees side by side. In an economy where margins are thin and every shilling matters, this is not a convenience — it is a competitive advantage.

The social commerce explosion

There is a particular form of entrepreneurship flourishing across Africa that Western business literature barely acknowledges: social commerce. Across Nigeria, Kenya, South Africa, Ghana, Egypt, and Tanzania, millions of entrepreneurs are running legitimate businesses entirely through WhatsApp, Instagram, and Facebook. They photograph products, post them to their stories, negotiate in DMs, arrange delivery through motorcycle riders, and collect payment via mobile money.

This is not informal trade in the dismissive sense that development economists sometimes use the term. This is sophisticated, customer-facing retail operating on platforms that happen not to have built-in accounting features. The result is that a seller in Nairobi doing fifty transactions a week often has no clear picture of their actual profit per item once delivery fees, packaging costs, platform advertising spend, and mobile money withdrawal charges are factored in.

The sociological dimension here matters. Many of these entrepreneurs, a disproportionate number of whom are women — have been told by formal financial institutions that their businesses are too small, too informal, or too risky. They have been excluded from the tools that larger businesses take for granted: inventory management, margin analysis, profit tracking. Yet these are precisely the businesses driving employment and economic participation across the continent.

The Social Commerce Profit Tracker was built for this reality. It lets a WhatsApp or Instagram seller input their product cost, selling price, delivery fee, ad spend, and packaging cost, and instantly see their true profit per item. It calculates break-even quantities. It runs on a phone. It requires no signup. This is not charity, it is infrastructure that should have existed a decade ago.

The multi-currency pricing problem

One of the most underestimated barriers to inter-Africa trade is the sheer complexity of pricing across currencies. Africa has over 40 actively traded currencies. A business in Accra that wants to sell to customers in Lagos, Nairobi, Johannesburg, and Dakar must price in Ghanaian cedis, Nigerian naira, Kenyan shillings, South African rand, and CFA francs, each with different exchange rate dynamics, different inflation profiles, and different levels of volatility.

Global currency tools were not built for this. They handle USD to EUR brilliantly. They handle NGN to KES poorly, if at all. And they certainly do not allow an entrepreneur to set a base price in one African currency and instantly generate retail prices across ten others with a margin built in.

The African Multi-Currency Pricing Calculator addresses this directly. It is a small thing, in one sense — just a calculator. But in another sense, it is an act of economic imagination: the assumption that an African entrepreneur’s primary market is other African countries, not Europe or America. That assumption, which would have seemed radical twenty years ago, is now simply the reality of where the growth is.

The import corridor opportunity

Let us speak plainly about one of the largest entrepreneurial activities on the continent: importation. Millions of African entrepreneurs import goods from China, Turkey, India, Dubai, and increasingly from other African countries. Consumer electronics from Shenzhen. Textiles from Istanbul. Auto parts from Mumbai. These goods flow into Apapa port in Lagos, Mombasa in Kenya, Tema in Ghana, Durban in South Africa.

The challenge is not finding goods to import. The challenge is calculating what those goods will actually cost once they clear customs. The landed cost — purchase price plus international shipping plus customs duty plus VAT plus clearing agent fees plus last-mile transport — is the number that determines whether an import business makes money or loses it. And yet most small importers calculate this on the back of an envelope, in a WhatsApp voice note to their clearing agent, or not at all.

The Import Duty & Landed Cost Calculator was built because this calculation should not require a customs broker. A trader should be able to input a product value, select a destination country, and see a clear breakdown of every cost component before they wire money to a supplier. That transparency is what separates a profitable import operation from a painful lesson.

What comes next

The trajectory is clear. Africa’s population will reach 2.5 billion by 2050. Its middle class is expanding faster than any other region. The AfCFTA is reducing barriers to intra-continental trade. Mobile money has created a payment infrastructure that bypasses legacy banking. And a generation of entrepreneurs — digital natives who think in WhatsApp catalogues and Instagram reels, is building businesses that would have been impossible fifteen years ago.

The question is not whether inter-Africa trade will grow. It will. The question is whether the tools, information, and infrastructure exist to let the small entrepreneur participate, not just the multinational with a compliance department and a correspondent banking relationship.

This is the work. Not glamorous. Not revolutionary in the way that manifestos are revolutionary. But deeply practical, and deeply Pan-African in its implications: the idea that an entrepreneur in Lusaka and an entrepreneur in Douala should be able to trade with each other as easily as they trade with London or Beijing. The tools to make that possible are not a luxury. They are a necessity.

And they should be free.